Frequently Asked Questions

This information does not, and is not intended to, provide legal, tax, or accounting advice to employers. The information provided here is general in nature and based on authorities that are subject to change. Readers should consult with their tax advisors concerning the application of tax laws to their particular situations.

FAQs About Health Connector for Business

FAQs about Options for Small Businesses to Manage Health Coverage Affordability

What are Health Connector for Business’s Employee Choice Models?

Employers can select different ways to offer coverage to their employees through Health Connector for Business. Employers can choose to offer either:

-

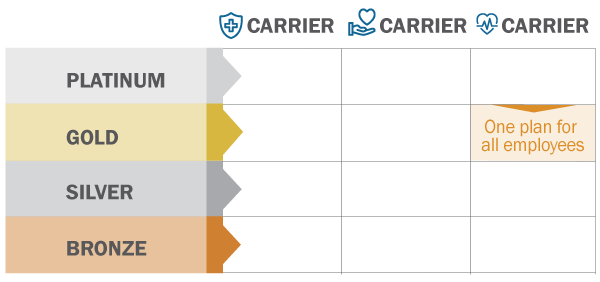

- One Plan: the employer chooses a plan and the company contribution amount. All employees can enroll in that one plan.

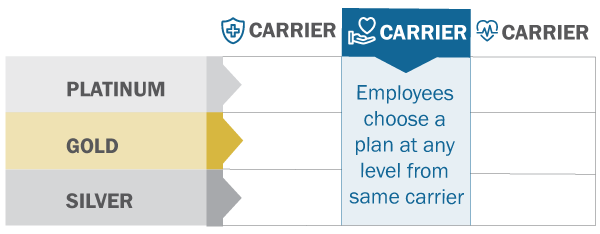

- One Carrier: the employer chooses an insurance carrier and company contribution amount. Employees can compare and choose a plan from that carrier at any benefit level to best meet their health care needs.

- One Plan: the employer chooses a plan and the company contribution amount. All employees can enroll in that one plan.

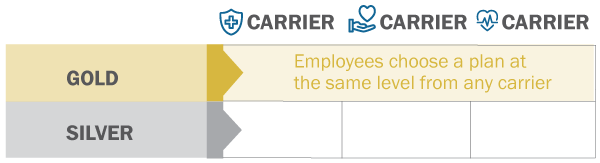

- One Level: the employer chooses a benefit level and company contribution amount. Employees can compare and choose among plans offered by a range of carriers at that benefit level.

With the option to select one plan, one carrier, or one level, Health Connector for Business is the only place in the small group market where small businesses can offer this degree of choice and flexibility to their employees. Please visit our Employee Choice page for more information.

How can I save 15 percent on premiums with ConnectWell?

ConnectWell is Health Connector for Business’ wellness rebate program that benefits both employers (with up to 25 employees) and their employees. If your group qualifies, employers can receive a 15 percent rebate on their contributions towards premiums for the plan year if one-third (33 percent) of their employees participate. Employees who participate in a qualified activity earn a $100 Visa gift card. Get more information about ConnectWell →

How can the Small Business Health Care Tax Credit help me save money and who is eligible to receive it?

Massachusetts-based small businesses can only claim the federal Small Business Health Care Tax Credit established under the Affordable Care Act if they buy coverage through Health Connector for Business. Since we are Massachusetts’s Small Business Health Options Program (“SHOP”), only small business employers that buy coverage through Health Connector for Business can apply for and claim this tax credit on their federal taxes.

The Small Business Tax Credit is worth up to 50 percent of for-profit employers’ annual premium contributions and up to 35 percent for tax-exempt employers’ annual premium contributions. In order to be eligible for the Small Business Health Care Tax Credit, businesses must:

- cover at least 50 percent of the cost of single (not family) health coverage for each employee;

- have fewer than 25 full-time equivalent employees (FTEs);

- have average annual wages per FTE that are under the limit set by the IRS each year (guidelines can be found on the most up to date IRS form 8941 and corresponding instructions); and

- shop through their state Marketplace (the Massachusetts Health Connector).

Please see the federal government’s SHOP calculator for assistance calculating Small Business Health Care Tax Credit eligibility. In addition, please see guidance from the IRS for additional information about the Small Business Health Care Tax Credit and eligibility.